Newsroom

Welcome on Groupe Credit Agricole Newsroom

06-08-2020

Results for the second quarter and first half of 2020

A V-shaped recovery for Crédit Agricole Group

Crédit Agricole Group

Largest bank in France, the Group is massively committed to supporting the economy

The crisis has brought the Group even closer to its customers. Substantial support measures were introduced to stay in contact with them. 9 out of 10 branches and advisers throughout the Group’s retail banking network could be contacted during the lockdown period, either in person or remotely. At CA Italia, there was a significant increase in remote interactions, with +30% of customers active online. For the Regional Banks, the growth rate for digital customers was up +0.8 of a percentage point.

The Group’s strong efforts throughout this challenging period are also reflected in its support for its hardest-hit customers. The Group has been aligned from the outset with government strategies, with targeted measures for each customer category, and therefore continues to meet its customers’ needs. On 6 March, Crédit Agricole Group granted a six-month moratorium on loan repayments for corporate, SME and small business customers impacted by COVID-19. As at 17 July 2020, a total of 552,000 moratoria was granted in French retail banking for a total amount of €4.2 billion in extended maturities (of which, 83% for SMEs, small businesses, and Corporates, 71% at the Regional Banks and 29% at LCL). The French government also announced the introduction on 25 March of State guaranteed loans (Prêts Garantis par l’Etat) to meet the cash flow requirements of businesses impacted by the coronavirus crisis. By virtue of its strong regional presence and universality, the Group supports all businesses, from the smallest company to the largest corporation, and to date has received 23.7% of all State guaranteed loan requests. As at 24 July 2020, a total of 179,500 applications had been received by the Group for an amount of €28.7 billion (of which 62% for Regional Banks, 30% for LCL and 8% for Crédit Agricole Corporate and Investment Bank). The Group has provided specific support to its SME and small business customers insured against business interruption, with mutualistic support totalling €239 million. Lastly, €2 billion of moratoria and State Guaranteed loans have been provided to CA Italia’s customers.

Being available and receptive to its most disadvantaged customers has been a key priority for the Group in recent months, as the number of customers in a vulnerable situation rose significantly. The Group has responded by offering exemptions from penalty and overdraft facilities for SMEs and small businesses at the Regional Banks and LCL.

In the current context, the Group Project is more than ever proving its relevance. With regards to the Customer Project, the intensification of the relationship with customers has been reflected in their feedback and the Group is seeing an increase in its NPS4 (Net Promoter Score) across all networks in 2020: +8 points for the Regional Banks (+7 points vs. 2019), +2 points for LCL (+7 points vs. 2019) and improvement of customer satisfaction for CA Italia. The Group is also continuing to steer its distribution and relationship model towards greater digitisation. Examples of this during the quarter include the increase in the contactless payment limit from €30 to €50 rolled out in six weeks, electronic signature of State guaranteed loan applications for SME and small business customers in Retail banking, paperless property and casualty insurance claims, and automatic processing of moratoria applications at CAL&F. The Human Project has been further strengthened, first and foremost by the total commitment of all employees to support customers, whether or not they have contact with them. Exceptional delegations have been set up in branches, illustrating the Group’s sense of local responsibility. During the crisis, customers have demonstrated a greater appetite for ESG offerings, which has made the Group even more determined to step up its community involvement through the Societal Project. At end-June, it introduced a non-financial reporting platform at Group level to meet the challenges of implementing and managing the Group’s societal targets. The approaches of the Crédit Agricole S.A. sub-divisions are also aligned with the Group’s community involvement, which has led to the launch of the first global equity fund focused on reducing inequalities for Amundi and the first complete range of asset investments in the fight against global warming for LCL. Crédit Agricole Corporate and Investment Bank, meanwhile, ranks Number 1 globally for social and green bonds. The Group is also very focused on diversity and youth employment and is determined to achieve its targets in these areas. Specifically, it has pledged to employ 4,000 work/study employees in 2020 (which places it in the Top 2 of the Figaro/Cadremploi ranking) and is making good process in the SBF 120's ranking of women in decision-making bodies, moving up 46 places in 2020 to rank in the Top 50. All of this attests to the accelerated roll-out of the Group Project's three Pillars.

The Group’s commercial activity in the quarter was good, but especially buoyant at the end of the period. AuMs were up from second quarter 2019 (+7.1%), as were those of life insurance (+1.6%) with a rise in the percentage of unit-linked assets (+0.5 percentage point between June 2019 and June 2020 to 22.7%). In the retail banking networks in France and Italy, growth in outstandings remained strong. Loans outstanding amounted to €726.9 billion (€681.8 billion in France and €44.2 billion in Italy; €708.4 billion excluding State guaranteed loans), up +8.7% from second quarter 2019 (+9% in France and +4.9% in Italy), and up +5.9% excluding State guaranteed loans. On-balance sheet deposits stood at €671.8 billion, up +11% from second quarter 2019, while off-balance sheet deposits remained stable (+0.1% at €382.8 billion). Gross customer capture was particularly solid (+685,000 customers in 2020, of which 630,000 in France and 55,000 in Italy), with a sharp acceleration in June (+150,000 customers, +2.4% June/June). Against this backdrop, the customer base continued to grow significantly (+38,000 additional customers in 2020, of which 36,500 in France and 1,500 in Italy, +4.4% June/June). Consolidated consumer finance loans were stable (+0.2%), with sales regaining momentum in June (+170% between April and June 2020). Lastly, business in the Large Customers business line was extremely buoyant, especially in capital markets (revenues up +44% from second quarter 2019), with all sub-divisions making a strong contribution. Financing activities also posted good revenue growth (+6%) due to its ability to mobilise the full range of financing solutions for customers.

Group results

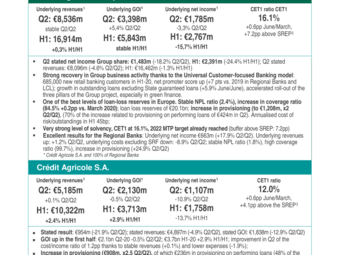

In the second quarter of 2020, Crédit Agricole Group’s stated net income Group share amounted to €1,483 million, versus €1,813 million in second quarter 2019. The specific items recorded in the quarter generated a net negative impact of -€302 million on net income Group share.

Specific items, this quarter (-€302 million on net income Group share), included the impact of the cooperative support given to SME and small business customers with business interruption insurance amounting to ‑€94 million in Regional Bank revenues, -€2 million in LCL revenues and -€143 million in insurance revenues (impact on net income Group share of ‑€64 million, -€1 million and -€97 million respectively), as well as the impact of the cash adjustment on the Liability Management transaction carried out by Crédit Agricole S.A. at the beginning of June 2020 (-€41 million in revenues and -€28 million in net income Group share). The recurring accounting volatility items are to be added with a net negative impact of -€160 million in revenues and ‑€109 million in net income Group share, namely DVA (Debt Valuation Adjustment, i.e. gains and losses on financial instruments related to changes in the Group’s issuer spread), in addition to which the Funding Valuation Adjustment (FVA) portion associated with the change in the issuer spread, which is not hedged, totalling -€5 million, the hedge on the Large Customers loan book amounting to -€51 million, and the change in the provision for home purchase savings plans amounting to -€53 million. Specific items also include integration costs for entities recently acquired by CACEIS (Kas Bank and S3) for ‑€5 million in operating expenses and -€2 million in net income Group share. The activation of the Switch guarantee in second quarter 2020 generated two opposite impacts on cost of risk amounting to €65 million in the Asset Gathering business lines (positive impact) and for the Regional Banks (‑€65 million). In the second quarter 2019, specific items had had a net negative impact of ‑€33 million on net income Group share; they included only recurring accounting volatility items such as the Debt Valuation Adjustment (DVA, i.e. gains and losses on financial instruments related to changes in the Group’s issuer spread) amounting to -€3 million, the hedge on the Large customers loan book for -€6 million, and the changes in the provisions for home purchase savings schemes in the amount of ‑€24 million.

Excluding these specific items, the underlying net income Group share5 was €1,785 million, down -3.3% compared to second quarter 2019. This decline was mainly due to the effects of the COVID-19 crisis, particularly on outstanding loan provisioning.

- Underlying, excluding specific items. See p.32 and onwards for more details on specific items.

- Based on SREP requirement of 7.9%

- Based on SREP requirement of 8.9%

- National Net Promoter Score for individuals in 2020: difference between promoters and detractors

- Underlying, excluding specific items. See p.32 and onwards for more details on specific items.

(Web) CASA Q2 press conf ENG.pdf

06-08-2020

EN_CASA_2020-Q2_PR.pdf

06-08-2020

Our linked press release